[ad_1]

Earlier, I highlighted some of the so-termed ‘reopening trades’ that remain on the JSE (There are nonetheless ‘reopening trades’ out there), which bundled Spur Corporation (SUR).

Spur has now produced its interim benefits for the six months to 31 December 2022, revealing just how perfectly it is accomplishing – and the share value has started off responding positively.

Read through:

How substantially more upside may be left?

Spur Corp observed its H1:23 restaurant turnover increase 31.5%, driving group earnings up 35% and doubling financial gain just before tax.

Headline earnings for each share (Heps) followed suite, with a 198% rise (similar Heps was up 81% yr on 12 months), which management employed to hike its dividend 67%.

The group’s stability sheet remains internet funds with no gearing, team dollars flows stay powerful, and core running expenses had been tightly managed – and, as much as I can explain to, continue to be beneath pre-Covid levels (in other words, exiting the pandemic leaner and fitter as a team).

Supply: The writer

While supply chains are continue to normalising (although they are much far better than prior to, with the exception perhaps of rooster), the group was most likely a web beneficiary of load shedding.

Study:

Having difficulties to get chicken at your closest speedy meals chain?

KFC SA to near some models owing to electric power cuts

A entire 95% of its suppliers run on turbines (with managing expenses of only .5% to 2.6%), with inverters, battery and photo voltaic setups there way too.

Thus, when consumers are load-lose all over mealtimes, Spur – becoming Spur, RocoMamas, Panarottis, John Dory’s, The Hussar Grill, and a few of other brands – is a viable choice.

Read: SA’s retail and quick-foods giants demand tax relief from governing administration

This is primarily accurate if you have kids (Spur completely dominates in the loved ones restaurant market place), but also if you are employing Uber Eats or Mr D for deliveries.

On this latter position, it was good to see Spur management using digital kitchen (VK) brand names like Just Wingz, Pizza Pug and Bento to generate incremental profits.

These incremental gross sales leverage the group’s existing store footprint, incorporating significant-margin revenues to existing fastened charges that should really cascade down the group’s earnings statement. Also, I suppose, if any of these VK brand names seriously acquire off, the team can commence to roll out distinct dining establishments for the brands.

Resource: The creator

This is all optimistic, and regardless of stress on purchaser disposable income, Spur is perfectly-positioned going ahead with quite a few levers to pull to extract profitable progress.

But how does the share’s valuation glance?

The group’s share’s rolling 10-12 months common value-earnings (PE) ratio is 176 situations. Even when compared against a person common deviation below this common, its meagre 11.6 moments existing PE is very low. Exceptionally very low.

But the planet has transformed, the South African environment has come to be more durable, and curiosity charges have risen (which should benefit ungeared organizations, by the way!).

Perspective

How does Spur stack up in opposition to its global friends, and community rival Well known Brands?

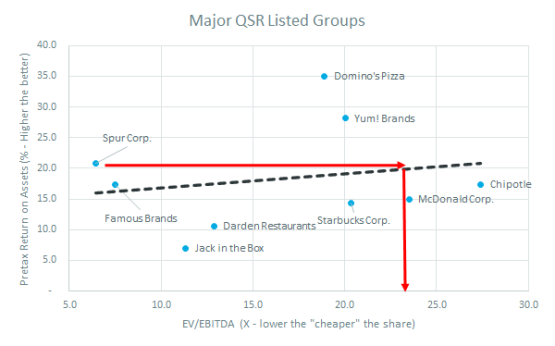

Regardless of remaining considerably scaled-down, Spur (and in truth Famous Brand names) compare quite well towards important world-wide QSR (brief support restaurants) and ordinary restaurant chains that are outlined.

Equally have pre-tax (critical to use pre-tax, as other geographies have different tax charges) returns on property that are greater than most QSR groups.

Apparently, the two are also much cheaper when in contrast in opposition to their EV/Ebitda (company price/earnings ahead of desire, tax, depreciation and amortisation) ratio – which is kind of like a PE ratio, but manages for unique value structures and neutralises different amounts of debt to make it far more globally similar.

Now, if we statistically uncover the ‘line of best fit’ (linear regression) monitoring these shares, the market tends to pay out a lot more for QSR shares that are a lot more successful. In other words, larger EV multiples on their Ebitda from bigger pre-tax returns on property (ROAs).

Well-known Brands is not just considerably less successful than Spur (decrease pre-tax ROA), but its valuation is sitting down relaxed on the line of very best suit. This indicates that Renowned Brand names is appropriately valued in opposition to this peer established.

Opposing this, Spur Corporation’s superior pre-tax ROA implies that it should really be materially greater-valued (stick to the purple line to wherever its share’s valuation would sit and this implies its EV/Ebitda many). In simple fact, if you observe this logic by, Spur’s valuation (and, for this reason, its share rate) must be a tiny above two-and-a-50 % instances higher – on an EV/Ebitda approaching 23 situations!

Consequently, the evidence (better than a standard deviation undervalued in opposition to record and out of kilter with world friends) is that Spur Corp’s shares remain fairly comfortably undervalued despite its constructive prospective clients.

The remedy as a result to how considerably extra upside may be remaining in Spur shares is ‘Could be rather a lot’!

Hear to host Simon Brown and Chantal Marx of FNB Prosperity and Investments unpack the buying and selling update issued by Spur Company in February:

You can also hear to this podcast on iono.fm below.

* Some of portfolios managed by Integral Asset Administration may well keep Spur Corp shares.

Keith McLachlan is main investment officer at Integral Asset Management.

[ad_2]

Source url